Last Update 3 hours ago Total Questions : 268

The F2 Advanced Financial Reporting content is now fully updated, with all current exam questions added 3 hours ago. Deciding to include F2 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our F2 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these F2 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any F2 Advanced Financial Reporting practice test comfortably within the allotted time.

On 1 January 20X4 JK had 1,500,000 ordinary shares in issue. On 1 September 20X4 JK issued 600,000 ordinary shares at the market value of $2.50 a share. For the financial year ended 31 December 20X4 the statement of profit or loss shows profit before tax of $625,000 and profit after tax of $500,000.

What is the earnings per share for the year ended 31 December 20X4?

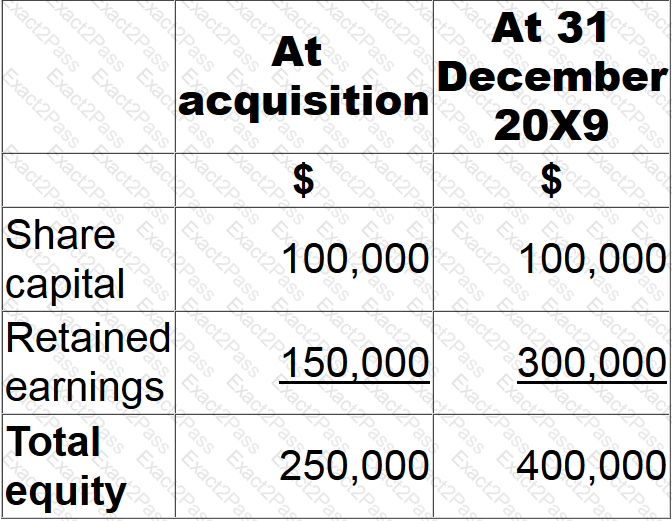

ST owns 75% of the equity share capital of GH. GH owns 80% of the equity share capital of RS.

The following balances relate to RS:

The non controlling interest in respect of RS had a fair value of $56,000 at acquisition. There has been no impairment to goodwill since acquisition.

What value should be included in ST ' s consolidated statement of financial position for the non controlling interest in RS at 31 December 20X9?

LK acquired 100% of the equity shares of TU on 1 January 20X4. LK disposed of 60% of TU for £2,400,000 on 30 September 20X4. The sale proceeds reflected the fair value of TU ' s shares on that date.

The remaining 40% shareholding gave LK the ability to exercise significant influence over the activities of TU. TU reported profit of $1,800,000 for the year ended 31 December 20X4 and this accrued evenly throughout the year.

Calculate the investment in associate that will be presented in LK ' s consolidated statement of financial position as at 31 December 20X4.

Give your answer to the nearest whole $ ' 000.

$ 000

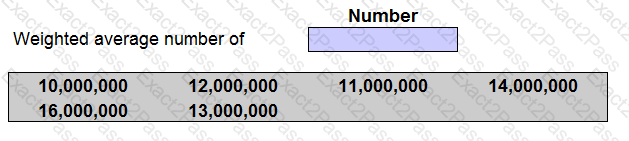

On 1 January 20X8 XY, a listed entity, had 10,000,000 ordinary shares in issue each with a par value of 50 cents. On 1 July 20X8 XY raised $6,000,000 by issuing ordinary shares at a price of £1.50 each which was the full market price.

Place the correct figure into the box below to show the number that XY will use as its weighted average number of ordinary shares in the calculation of earnings per share for the year to 31 December 20X8.

AB acquired an investment in a debt instrument on 1 January 20X5 at its nominal value of $25,000, which it intends to hold until maturity. The instrument carried a fixed coupon interest rate of 5%, payable in arrears. Transactions costs of $5,000 were paid in respect of this investment. The effective interest rate applicable to this instrument was estimated at 9%.

Calculate the value of this investment that AB will include in its statement of financial position at 31 December 20X5.

Give your answer to the nearest whole number.

$ ?

FG granted share options to its 500 employees on 1 August 20X0. Each employee will receive 1,000 share options provided they continue to work for FG for the four years following the grant date. The fair value of the options at the grant date was $1.30 each. In the year ended 31 July 20X1, 20 employees left and another 50 were expected to leave in the following three years. In the year ended 31 July 20X2, 18 employees left and a further 30 were expected to leave during the next two years.

The amount recognised in the statement of profit or loss for the year ended 31 July 20X1 in respect of these share options was $139,750.

Calculate the charge to FG ' s statement of profit or loss for the year ended 31 July 20X2 in respect of the share options.

FG acquired 75% of the equity share capital of HI on 1 September 20X3.

On the date of acquisition, the fair value of the net assets was the same as the carrying amount, with the exception of a contingent liability disclosed by HI and relating to a pending legal case. At 1 September 20X3, the contingent liability was independently valued at $1.2 million.

At the current year end, 31 March 20X5, the legal case is still outstanding. The fair value of the liability has now been estimated at $1.4 million, and the case is expected to be resolved in the forthcoming financial year.

How should this contingent liability be recorded in the consolidated financial statements for the year ended 31 March 20X5?